Introduction #

Options trading may seem overwhelming at first, but it’s easy to understand if you know a few key points. Investor portfolios are usually constructed with several asset classes. These may be stocks, bonds, ETFs, and even mutual funds. Options are another asset class, and when used correctly, they offer many advantages that trading stocks and ETFs alone cannot.

Disclaimer: Options involve risks and are not suitable for everyone. Options trading can be speculative in nature and carry substantial risk of loss.

Options are contracts that give the bearer the right, but not the obligation, to either buy or sell an amount of some underlying asset at a pre-determined price at or before the contract expires. Options can be purchased like most other asset classes with brokerage investment accounts.

Options are powerful because they can enhance an individual’s portfolio. They do this through added income, protection, and even leverage. Depending on the situation, there is usually an option scenario appropriate for an investor’s goal. A popular example would be using options as an effective hedge against a declining stock market to limit downside losses. Options can also be used to generate recurring income. Additionally, they are often used for speculative purposes such as wagering on the direction of a stock.

There is no free lunch with stocks and bonds. Options are no different. Options trading involves certain risks that the investor must be aware of before making a trade. This is why, when trading options with a broker, you usually see a disclaimer similar to the following:

Options as Derivatives #

Options belong to the larger group of securities known as derivatives. A derivative’s price is dependent on or derived from the price of something else. Options are derivatives of financial securities—their value depends on the price of some other asset. Examples of derivatives include calls, puts, futures, forwards, swaps, and mortgage-backed securities, among others.

Why Choose Options #

Investors and traders undertake option trading either to hedge open positions (for example, buying puts to hedge a long position, or buying calls to hedge a short position) or to speculate on likely price movements of an underlying asset.

The biggest benefit of using options is that of leverage. For example, say an investor has $900 to use on a particular trade and desires the most bang-for-the-buck. The investor is bullish in the short term on XYZ Inc. So, assume XYZ is trading at $90. Our investor can buy a maximum of 10 shares of XYZ. However, XYZ also has three-month calls available with a strike price of $95 for a cost $3. Now, instead of buying the shares, the investor buys three call option contracts. Buying three call options will cost $900 (3 contracts x 100 shares x $3).

Shortly before the call options expire, suppose XYZ is trading at $103 and the calls are trading at $8, at which point the investor sells the calls. Here’s how the return on investment stacks up in each case.

- Outright purchase of XYZ shares at $90: Profit = $13 per share x 10 shares = $130 = 14.4% return ($130 / $900).

- Purchase of three $95 call option contracts: Profit = $8 x 100 x 3 contracts = $2,400 minus premium paid of $900 = $1500 = 166.7% return ($1,500 / $900).

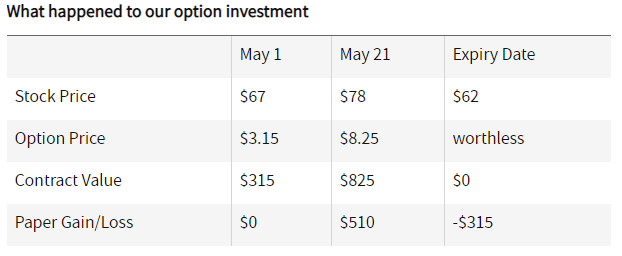

Of course, the risk with buying the calls rather than the shares is that if XYZ had not traded above $95 by option expiration, the calls would have expired worthless and all $900 would be lost. In fact, XYZ had to trade at $98 ($95 strike price + $3 premium paid), or about 9% higher from its price when the calls were purchased, for the trade just to breakeven. When the broker’s cost to place the trade is also added to the equation, to be profitable, the stock would need to trade even higher.

These scenarios assume that the trader held till expiration. That is not required with American options. At any time before expiry, the trader could have sold the option to lock in a profit. Or, if it looked the stock was not going to move above the strike price, they could sell the option for its remaining time value in order to reduce the loss. For example, the trader paid $3 for the options, but as time passes, if the stock price remains below the strike price, those options may drop to $1. The trader could sell the three contracts for $1, receiving $300 of the original $900 back and avoiding a total loss.

The investor could also choose to exercise the call options rather than selling them to book profits/losses, but exercising the calls would require the investor to come up with a substantial sum of money to buy the number of shares their contracts represent. In the case above, that would require buying 300 shares at $95.

Speculation #

Speculation is a wager on future price direction. A speculator might think the price of a stock will go up, perhaps based on fundamental analysis or technical analysis. A speculator might buy the stock or buy a call option on the stock. Speculating with a call option—instead of buying the stock outright—is attractive to some traders since options provide leverage. An out-of-the-money call option may only cost a few dollars or even cents compared to the full price of a $100 stock.

Hedging #

Options were really invented for hedging purposes. Hedging with options is meant to reduce risk at a reasonable cost. Here, we can think of using options like an insurance policy. Just as you insure your house or car, options can be used to insure your investments against a downturn.

Imagine that you want to buy technology stocks. But you also want to limit losses. By using put options, you could limit your downside risk and enjoy all the upside in a cost-effective way. For short sellers, call options can be used to limit losses if the underlying price moves against their trade—especially during a short squeeze.

How Are Options Valued #

In terms of valuing option contracts, it is essentially all about determining the probabilities of future price events. The more likely something is to occur, the more expensive an option would be that profits from that event. For instance, a call value goes up as the stock (underlying) goes up. This is the key to understanding the relative value of options.

The less time there is until expiry, the less value an option will have. This is because the chances of a price move in the underlying stock diminish as we draw closer to expiry. This is why an option is a wasting asset. If you buy a one-month option that is out of the money, and the stock doesn’t move, the option becomes less valuable with each passing day. Since time is a component to the price of an option, a one-month option is going to be less valuable than a three-month option. This is because with more time available, the probability of a price move in your favor increases, and vice versa.

Accordingly, the same option strike that expires in a year will cost more than the same strike for one month. This wasting feature of options is a result of time decay. The same option will be worth less tomorrow than it is today if the price of the stock doesn’t move.

Volatility also increases the price of an option. This is because uncertainty pushes the odds of an outcome higher. If the volatility of the underlying asset increases, larger price swings increase the possibilities of substantial moves both up and down. Greater price swings will increase the chances of an event occurring. Therefore, the greater the volatility, the greater the price of the option. Options trading and volatility are intrinsically linked to each other in this way.

On most U.S. exchanges, a stock option contract is the option to buy or sell 100 shares; that’s why you must multiply the contract premium by 100 to get the total amount you’ll have to spend to buy the call.

The majority of the time, holders choose to take their profits by trading out (closing out) their position. This means that option holders sell their options in the market, and writers buy their positions back to close. Only about 10% of options are exercised, 60% are traded (closed) out, and 30% expire worthlessly.

Fluctuations in option prices can be explained by intrinsic value and extrinsic value, which is also known as time value. An option’s premium is the combination of its intrinsic value and time value. Intrinsic value is the in-the-money amount of an options contract, which, for a call option, is the amount above the strike price that the stock is trading. Time value represents the added value an investor has to pay for an option above the intrinsic value. This is the extrinsic value or time value. So, the price of the option in our example can be thought of as the following:

In real life, options almost always trade at some level above their intrinsic value, because the probability of an event occurring is never absolutely zero, even if it is highly unlikely.